Maximize Your 2026 Depreciation Deductions

Turn Business Purchases into Tax Savings

Depreciation deductions are among the most powerful tax tools for business owners. They let you write off the cost of equipment, vehicles, software, and more over time. Recent tax law changes have changed first-year depreciation rules, making them even more generous, especially for new purchases placed in service this tax year.

This guide breaks down the first-year depreciation tax rules, how to claim them, and what’s changed under the new law.

What Is First-Year Depreciation?

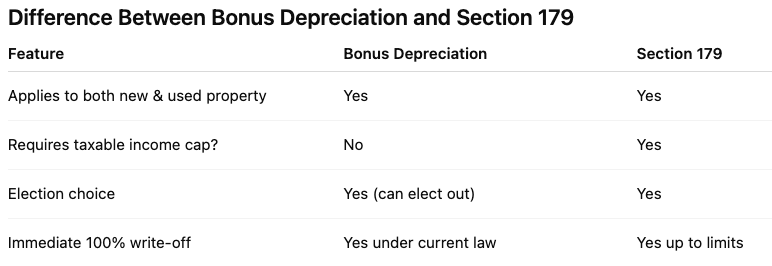

First-year depreciation refers to tax deductions you can take on the cost of business property in the same year you begin using it, rather than spreading that deduction over many years. The two primary ways to get these deductions are:

Bonus depreciation (also called “additional first-year depreciation”), or

Section 179 expensing.

These allow business owners to accelerate the tax benefit and reduce taxable income in the year that qualifying assets are placed in service.

Both tools can quickly lower taxable income, but your best strategy may be to use them in tandem.

Immediate Write-Off for Most Business Assets

Under the One Big Beautiful Bill Act (OBBBA), businesses can now claim 100% bonus depreciation on most qualified property acquired and placed in service after January 19, 2025. This means you can deduct the full cost of qualifying assets in the first year instead of depreciating them over several years.

What qualifies?

Equipment and machinery,

Computers and software,

Office furniture and fixtures,

Certain business vehicles used more than 50 percent for business, and

Qualified production property for manufacturers.

This applies whether the property is new or used, if it’s new to your business, and meets IRS qualifications.

Section 179 Deduction: Another First-Year Write-Off Option

Section 179 works alongside bonus depreciation but has its own rules. Under this provision, you can elect to expense the cost of qualifying property up to a limit in the year it’s placed in service.

2025 & 2026 Section 179 Highlights

Maximum first-year deduction of up to around $2.5 million for 2025 tax years.

The deduction begins to phase out once total eligible purchases exceed about $4 million.

Certain properties, such as roofs, HVAC systems, fire alarms, and security systems in nonresidential buildings, may also qualify.

Heavy SUVs (over 6,000-pound gross vehicle weight) may have special limits.

Unlike bonus depreciation, Section 179 deductions cannot exceed your business’s taxable income for the year, so planning matters.

Why This Matters for Your Business

Accelerated first-year depreciation can significantly reduce your tax bill. That means more cash stays in your business to reinvest in growth, hire talent, or buy crucial equipment.

Recent law changes restored and made permanent the 100% bonus depreciation benefit for most qualifying property placed into service after January 19, 2025. This restores one of the most valuable tax breaks for business owners and eliminates the uncertainty of prior phase-down schedules.

Common Mistakes to Avoid

Thinking all assets qualify: Some property, like certain building structures, doesn’t qualify for bonus depreciation.

Timing assets incorrectly: Purchase and in-service dates matter for qualification.

Ignoring the placed-in-service date: Your tax benefit starts when the asset is ready and available for use.

Ready to Optimize Your Tax Savings?

Depreciation rules are powerful but complex. Navigating bonus depreciation, Section 179, and vehicle limits can get confusing, especially around year-end planning. Your tax advisor can help determine the best mix of depreciation strategies tailored to your business goals.

Whether you’re investing in equipment, technology, vehicles, or building improvements, understanding and applying first-year depreciation rules could save your business thousands on taxes this year.

Contact our team today to see how you can take full advantage of these deductions before you file.