How the New Roth 401(k) Catch-Up Rules Impact Wealthier Savers

If you are 50 or older and saving for retirement, there’s an important update you need to know about your 401(k) plan for 2026. The rules for catch-up contributions are changing, especially for high earners. These changes could affect your taxes and retirement savings strategy.

Let’s break it down.

What Are Catch-Up Contributions?

Every worker who participates in a 401(k) plan has a yearly limit on how much they can save. But once you turn 50, you can contribute extra money beyond that limit. This extra amount is called a catch-up contribution. It helps you boost your retirement savings as you approach retirement age.

What’s Changing in 2026?

Starting in 2026, the government is making a big change to how catch-up contributions work for high earners:

According to Fidelity, if you are 50 or older and earn more than $150,000 in 2026, any catch-up contributions you make to your 401(k) must go into a Roth 401(k).

This rule comes from the SECURE 2.0 Act and is meant to shift more retirement savings into Roth accounts. It means:

· You put in after-tax dollars (you don’t get a tax break today).

· The money grows tax-free.

· You can take it out tax-free in retirement if you follow the rules.

How Does a Roth 401(k) Work?

A Roth 401(k) is a type of 401(k) where:

· You pay income tax on the money now.

· Your savings grow without being taxed.

· You don’t pay taxes when you take the money out in retirement.

· There are no required minimum withdrawals during your lifetime (unlike traditional 401(k)s).

This can be a significant benefit if you expect tax rates to rise in the future. It also gives you tax-free money later in life.

What the Rule Means for You

If you earned less than $150,000 in the prior year, you could still make catch-up contributions either:

· Pre-tax (traditional 401(k)), or

· After-tax (Roth 401(k)), if your plan allows it.

If you earned more than $150,000 in the prior year, you must contribute your catch-up dollars only to a Roth 401(k). You no longer get the pre-tax deduction you might be used to.

What if your plan doesn’t offer a Roth option?

If your employer does not offer a Roth 401(k), you won’t be able to make catch-up contributions under this rule. Some employers may need to change their plans to allow Roth 401(k) contributions.

Why This Matters

For high earners, the tax break you once enjoyed today for catch-ups is going away. But you still get tax-free growth on that money going forward.

This change affects retirement planning in a few ways:

1. You may pay more in taxes today, but

2. Your future retirement withdrawals from Roth funds can be tax-free, and/or

3. You may need to rethink how you save if you used catch-ups for tax breaks.

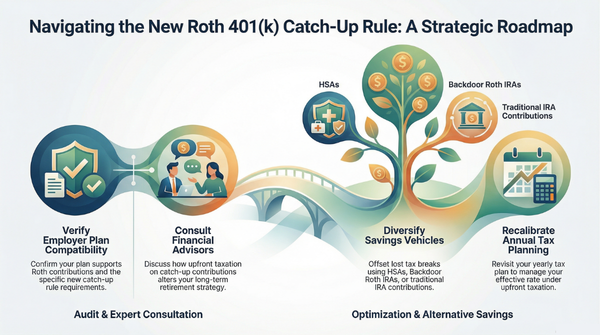

Next Steps for High-Net-Worth Clients

Here’s what you should consider doing now.

1. Review Your 401(k) Plan: Check whether your employer’s plan allows Roth 401(k) contributions and if it supports the new catch-up rule. If not, talk with the plan administrator about updates.

2. Work With a Financial Planner: Talk with your planner or tax advisor about how this change affects your overall retirement strategy, especially if you rely on catch-up contributions as part of your savings plan.

3. Maximize Other Savings Options: If you lose the tax break on catch-ups, consider:

Contributing to a Health Savings Account (HSA), if eligible,

Using a backdoor Roth IRA if you are over income limits, and/or

Planning for traditional IRA contributions for tax flexibility.

4. Revisit Your Tax Plan: Since catch-ups will be taxed upfront, now may be a good time to revisit your yearly tax planning to manage your effective tax rate.

Keep Building Toward a Secure Future

The 2026 Roth catch-up rule is a meaningful shift for high earners saving for retirement. It changes how catch-up contributions are taxed and where they must be placed. Knowing the rule and how it affects your retirement savings can help you plan smarter and keep building toward a secure future.

If you have questions or need personalized planning, contact your financial advisor, or we can help you make the most of these changes.